DIKA-MOKA YOUTH DEVELOPMENT FORUM.

Summary:

The system is structurally rigged to protect capital, not people. The Reserve Bank prints money for banks ("quantitative easing") to stabilize financial markets and protect asset-holders (e.g., banks, corporations, investors) because elites control the levers of economic power. Directly printing money for people—even though it would immediately alleviate poverty—is dismissed as "inflationary" or "fiscally irresponsible," despite the hypocrisy of doing the same for Wall Street or bailouts.

Why this double standard exists:

1. Power Dynamics: Banks and corporations wield political influence; the poor do not.

2. Inflation Fearmongering: Claims that "helicopter money" for the poor would cause hyperinflation ignore that inflation is already driven by corporate greed (e.g., price gouging, monopolies).

3. Wealth Protection: Printing for banks props up stock markets and property values (where the rich store wealth). Printing for people risks redistributing power—threatening the status quo.

The Truth:

The Reserve Bank could fund universal basic income or debt relief (as COVID stimulus proved). It chooses not to because the system exists to concentrate wealth, not democratize it. SARB’s policies primarily benefit established financial institutions, large corporations, and tech-driven enterprises that align with its mandates for stability and digital transformation. Smaller and informal businesses often face structural barriers despite government support programs. For a full list of initiatives, refer to SARB’s strategic focus areas

Systemic Root Causes of Inequality

· • Colonial & Apartheid Legacy: Historic land dispossession, racialized economic policy, migrant labor systems, segregated development.

· • Corporate Capture: Continued dominance by white-owned and foreign companies across finance, mining, agriculture, and retail.

· • False Transformation: B-BBEE fronting, selective empowerment of elites, and ineffective redistribution policies.

· • Neoliberal Fiscal Policy: Austerity, privatization, and liberalization weakened state control and excluded the poor.

· • Reserve Bank Mandate: Focus on inflation over employment reinforces elite financial stability over public investment.

· • Globalization: Favors multinational corporations and offshore profit extraction over local development.

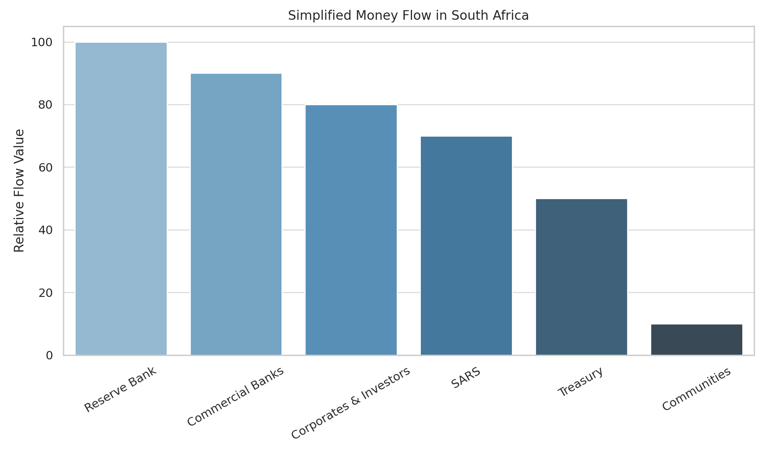

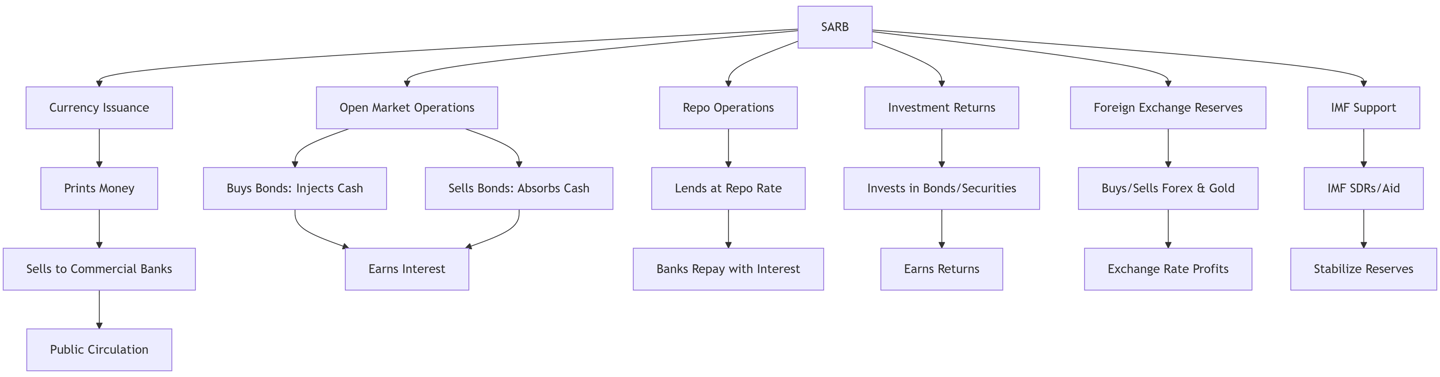

Money Flow Structure (Reserve Bank to Public)

· • Reserve Bank: Controls monetary policy, interest rates, and prints money. Lends to commercial banks.

· • Commercial Banks: Lend money mainly to established, large firms and wealthy individuals. Small black-owned businesses excluded.

· • SARS: Collects taxes — but high inequality persists due to evasions, loopholes, and regressive VAT burden on the poor.

· • Treasury: Distributes tax money — large allocations go to debt servicing, infrastructure for corporates, and SOEs.

· • Beneficiaries: Multinationals, institutional investors, and elite-consumer markets get the lion’s share of capital flow.

Companies and Communities That Benefit

· • Large Corporations: Anglo American, De Beers, Standard Bank, ABSA, FirstRand, Nedbank, Old Mutual, Remgro, Shoprite, Naspers, MTN, Sasol, etc.

· • Retail Chains: Woolworths, Pick n Pay, Checkers, Spar, Game — dominate township economies with supply chain control.

· • Mining Giants: Glencore, South32, Exxaro, Impala Platinum, Sibanye Stillwater, etc.

· • Asset Managers: Allan Gray, Coronation, PSG, Investec, Public Investment Corporation (PIC) — own shares across JSE.

· • Multinational Shareholders: BlackRock, Vanguard, JPMorgan Chase, Fidelity, and other US/UK/EU investment funds.

· • Communities Favored: Wealthy suburbs, mining towns, corporate nodes in Sandton, Stellenbosch, Cape Town, Durban North.

Shareholding, Race, Religion, and Regional Dynamics

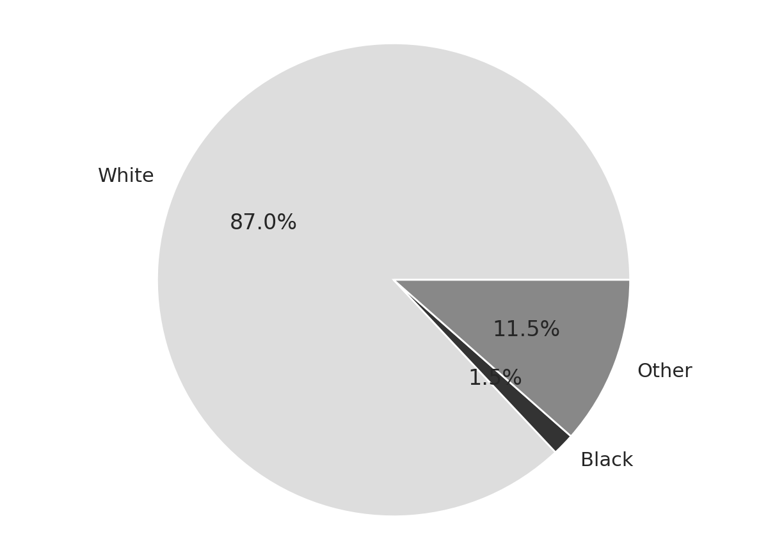

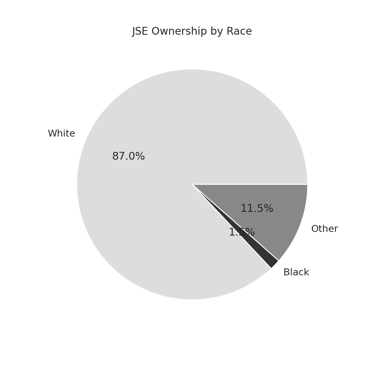

· • JSE Ownership: ~87% white, mostly institutional; <2% black direct ownership.

· • Top Management: 66% white-dominated, especially in finance, mining, manufacturing.

· • Regions: Gauteng (financial capital), Western Cape (retail/tech HQs), KZN (logistics, agriculture, chemical industries).

· • Religious Influence: Christian-majority country; Christian, Jewish, and secular financial communities dominate elite circles.

· • Wealth Disparity: Top 10% hold >85% of total wealth. Black rural and township communities remain structurally excluded.

Proposed Solutions for Justice and Reform

· • Cease All New Mining Licenses: Prevent ecological destruction, groundwater contamination, and land dispossession.

· • Community Ownership Models: Cooperatives, land trusts, and municipal enterprise support.

· • State-Led Banking: Nationalize at least one commercial bank to lend directly to communities and SMMEs.

· • Tax Justice: Close tax havens, penalize avoidance, and introduce wealth taxes on land and shares.

· • Land Redistribution: Return land to black communities via agrarian reform and food sovereignty programs.

· • Transparent Ownership: Public register of all large companies’ shareholders, demographics, and regions.

· • Youth-Led Green Economy: Support youth in agroecology, climate jobs, and zero-extraction innovation.

[ South African Reserve Bank ]

|

(Loans at repo rate)

↓

[ Commercial Banks ]

/ | \

(Loans to) (Buy bonds) (Invest)

↓ ↓ ↓

[Public] [Government] [Firms]

↓ ↓ ↑

[Taxes] [SARS → Treasury] |

↓ ↓ |

[Public pays VAT, fuel, income tax]

↓ ↓ |

[Treasury pays debt, tenders, services]

↓

[Wealthy Investors, Contractors]

Business beneficiaries of the SOUTH AFRICAN RESERVE BANK

Local Examples (Illustrative):

Information Technology (IT) Companies:

BCX: A large South African IT services provider.

Dimension Data (NTT Ltd.): A global technology services company with a significant presence in South Africa.

Adapt IT: A South African software and technology solutions company (now part of Volaris Group).

Consulting Firms:

PwC South Africa: A major professional services network.

Deloitte South Africa: Another large professional services firm.

Ernst & Young (EY) South Africa: A global professional services organization.

KPMG South Africa: A multinational professional services network.

McKinsey & Company: A global management consulting firm with an office in South Africa.

Boston Consulting Group (BCG): A global management consulting firm.

Security Services:

G4S South Africa: A large security services provider.

ADT Security: A well-known security company.

Fidelity Services Group: A major integrated security solutions provider.

Logistics and Transportation Companies:

SBV Services: Specializes in cash and valuable asset management and transportation.

Protea Coin Group: Offers cash management and logistics services.

Facilities Management Companies:

Bidvest Facilities Management: A large facilities management provider.

Servest: An integrated facilities solutions provider.

Professional Services (Legal & Audit):

Bowmans: A prominent African law firm.

ENSafrica: Another leading African law firm.

The "Big Four" audit firms (PwC, Deloitte, EY, KPMG) also provide audit services.

Communication and Marketing Agencies: Various agencies depending on specific projects.

Training and Development Providers: Numerous specialized training companies.

Printing and Stationery Suppliers: Various suppliers.

International Examples (Illustrative):

International Financial Institutions:

Bank for International Settlements (BIS): As a member, the SARB actively engages with the BIS.

International Monetary Fund (IMF): Interaction on policy and economic matters.

World Bank: Collaboration on development and financial stability issues.

Specialized Technology Vendors: Often multinational corporations with niche financial or security technologies. Specific names are less publicly known.

Global Financial Data and Information Providers:

Bloomberg L.P.: Provides financial data, news, and analytics.

Refinitiv (now part of LSEG): Another major provider of financial market data and infrastructure.

International Training Institutions: Universities and specialized financial training organizations based abroad.

Important Reminder:

This list provides examples of the types of companies and some well-known names that likely engage with the SARB. It is not an official or exhaustive list of all current or past business partners. The specific entities the SARB contracts with are subject to change based on their procurement needs and processes.

To get precise information about current suppliers, you would typically need to consult official tender publications and procurement announcements released by the SARB, if they choose to make that level of detail public.

Okay, let's try to provide some more names of companies that might engage with the South African Reserve Bank (SARB), keeping in mind the limitations of publicly available information. These are still illustrative examples based on the categories discussed:

More Local Examples (Illustrative):

Information Technology (IT) Companies:

EOH: Another large South African technology services provider.

T-Systems South Africa: A subsidiary of Deutsche Telekom providing IT services.

Bytes Technology Group: A significant IT company listed on the JSE and LSE.

Consulting Firms:

Oliver Wyman: A global management consulting firm.

Accenture South Africa: A multinational professional services company.

IQ Business: A South African management consulting firm.

Security Services:

Coin Security Group: Another provider of security and cash management solutions.

Servest Security: Part of the larger Servest group.

Logistics and Transportation Companies:

Smaller, specialized logistics companies for specific transport needs.

Facilities Management Companies:

Aramark South Africa: Provides facilities management services.

Smaller, niche facilities management providers.

Professional Services (Legal & Audit):

Webber Wentzel: A prominent South African law firm.

Cliffe Dekker Hofmeyr: Another leading South African law firm.

Smaller, specialized legal and auditing practices.

Communication and Marketing Agencies: Various smaller and specialized agencies for specific campaigns or projects.

Training and Development Providers: Numerous niche training providers focusing on finance, economics, or security.

Printing and Stationery Suppliers: Smaller, local printing companies and stationery suppliers.

More International Examples (Illustrative):

Specialized Technology Vendors: Companies specializing in:

Core Banking Systems: Providers like Temenos or Finastra (though local banks are the direct clients).

Payment Processing Technologies: Global providers of payment infrastructure.

Cybersecurity Solutions: International cybersecurity firms.

Economic Modeling Software: Vendors of specialized software for economic forecasting.

Global Financial Data and Information Providers:

S&P Global: Provides financial information and analytics.

Moody's Analytics: Offers financial intelligence and analytical tools.

International Training Institutions: Universities with strong finance or economics departments offering executive education, or specialized central banking training programs.

Foreign Central Bank Service Providers: Companies that provide specialized services to central banks (e.g., banknote design or production technology, though often highly confidential).

Continued Reminder:

This expanded list is still based on logical assumptions about the types of services a central bank like the SARB would require. The specific names of companies the SARB currently contracts with are not generally public knowledge. Official procurement channels and announcements would be the primary source for such information, if released.

The South African Reserve Bank (SARB) collaborates with a diverse array of local and international entities across various sectors, including banking, insurance, and foreign exchange. Below is an overview of these partnerships:

South African Registered Banks

SARB regulates and supervises numerous commercial banks operating within South Africa. Notable institutions include:

Absa Bank Limited

African Bank Limited

Bidvest Bank Limited

Capitec Bank Limited

Discovery Bank Limited

FirstRand Bank Limited

Investec Bank Limited

Nedbank Limited

Standard Bank of South Africa Limited

TymeBank Limited

Foreign Banks Operating in South Africa

Several international banks have a presence in South Africa, either as subsidiaries or representative offices. These include:

Bank of China

Citibank

Deutsche Bank

HSBC

JPMorgan Chase

Standard Chartered Bank

Authorised Dealers in Foreign Exchange

SARB designates certain financial institutions as Authorised Dealers, permitting them to conduct foreign exchange transactions. These dealers are crucial for facilitating international trade and investment. (finglobal.com)

Authorised Dealers with Limited Authority (ADLAs)

ADLAs are entities authorised to perform specific foreign exchange transactions, such as:

Travel-related transactions

Money remittance services

Facilitating transactions within prescribed limits(finglobal.com)

These institutions play a vital role in providing accessible foreign exchange services to the public.

Registered Insurers

SARB oversees a range of insurance companies operating within South Africa, including:

AECI Captive Insurance Company Limited

Affinity Life Limited

African Rainbow Life Limited

These insurers offer various life and non-life insurance products and are regulated to ensure financial stability and consumer protection.

Ownership and Shareholding

Private Ownership: SARB is one of the few central banks globally that is privately owned. It has issued 2 million shares, held by approximately 800 private shareholders, including both South African and international individuals and entities. Notable shareholders include Absa, the Anton Rupert Trust, Discovery, and FirstRand Bank.

Shareholding Limits: No single shareholder is permitted to own more than 10,000 shares. Shareholders receive a fixed annual dividend of 10 South African cents per share, with the remainder of the profits transferred to the South African government.

Nationalization Plans: The South African government has announced intentions to nationalize the Reserve Bank, aiming to bring it under full state ownership.

Explanation of the Flow:

Government (National Budget, Taxes): The primary source of funding is the government, which collects revenue through taxes (income tax, VAT, corporate tax, etc.). This revenue is allocated to various government departments and forms the national budget.

Government Funding Institutions: A portion of the national budget is channeled to various government funding institutions (like the IDC, NEF, SEFA, NSFAS, etc.). These institutions act as intermediaries to distribute funds according to their specific mandates.

Companies (Various Sectors): Government funding institutions provide financial support (loans, grants, incentives) to companies across different sectors to stimulate economic growth, job creation, and specific policy objectives (e.g., BEE, innovation).

Individuals (Students, Entrepreneurs, Citizens): Institutions like NSFAS provide direct financial assistance to individuals for education. Others may support entrepreneurs or provide social benefits indirectly.

Non-Governmental Organizations (NGOs): Some government funding is directed towards NGOs that work on various social development issues and provide services to specific communities.

Employees (Salaries, Wages): Companies that receive government funding use some of it to pay salaries and wages to their employees, benefiting individuals and households.

Shareholders (Dividends): Profitable companies may distribute dividends to their shareholders, who can be individuals or other institutions.

Government (Taxes, Repayments): Companies contribute back to the government through taxes on profits and repayments of loans received from funding institutions.

Education, Housing, Basic Needs, Entrepreneurship: Individuals who receive funding (e.g., students) use it for education, while entrepreneurs might use it to start businesses, contributing to economic activity and potentially creating jobs.

Beneficiaries (Specific Groups in Need): NGOs use government funding to support their target beneficiaries, addressing various social needs.